Why the Longevity Economy Is the Defining Industry of Our Era

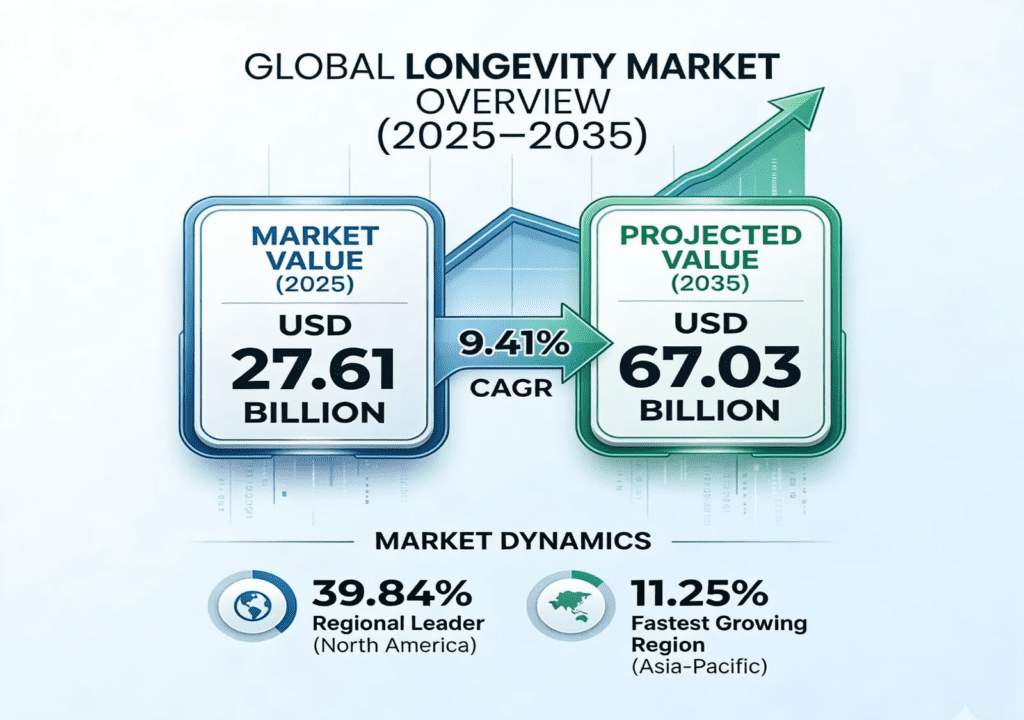

The way we think about aging is changing — not gradually, but fundamentally. What was once an inevitable biological countdown is now the target of the most sophisticated convergence of science, technology, and capital the healthcare world has ever seen. The numbers confirm what forward-thinking practitioners and investors already sense: the global longevity market, valued at USD 27.61 billion in 2025, is on a trajectory to reach USD 67.03 billion by 2035. That is not merely growth. That is a structural transformation of human health.

At Longevor, we sit at the intersection of this transformation — and we believe understanding the forces shaping this market is essential for anyone serious about optimizing healthspan, not

From Disease Management to Biological Capital

The longevity economy is not an extension of traditional healthcare. It is a departure from it.

Conventional medicine is organized around the treatment of disease after it manifests. The longevity paradigm inverts this entirely, focusing on the proactive modulation of biological aging processes — intervening at the cellular, genomic, and metabolic level before dysfunction has a chance to compound.

This shift is reflected in who is driving the market. In 2025, the individual consumer segment accounted for 35.12% of total market share — the single largest cohort — outpacing institutional healthcare buyers. People are no longer waiting for a diagnosis. They are investing in their biological capital, directly and deliberately. The direct-to-consumer channel commanded 32.23% of distribution, with online platforms projected to grow at a 12.25% CAGR through 2035.

The Science Driving the Economics

Growth of this magnitude is not speculative. It is anchored in concrete scientific breakthroughs that are now crossing the threshold from laboratory to clinical and commercial viability.

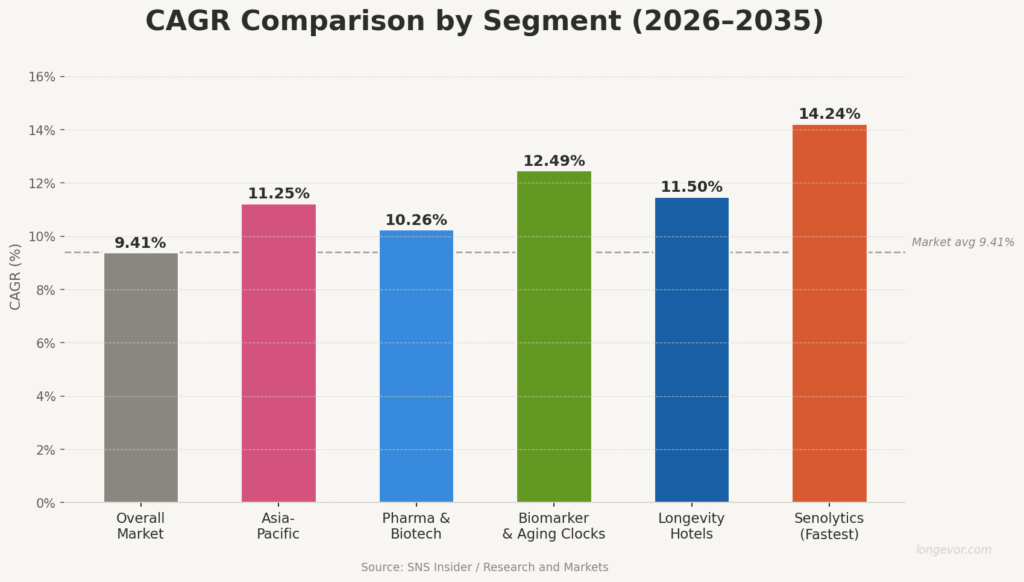

Senolytics and senotherapeutics — compounds that selectively remove senescent “zombie” cells that accumulate with age and accelerate systemic decline — represent the fastest-growing product category in the sector, projected at a 14.24% CAGR through 2035. This is targeted biological intervention at a level that was theoretical a decade ago. It is now in trials.

Genomics and epigenetics led the precision diagnostics landscape in 2025 with a 24.25% market share, enabling clinicians to identify genetic predispositions and track DNA methylation patterns that serve as reliable proxies of biological age. Alongside this, biomarker and aging clock technologies are projected to grow at 12.49% CAGR because what gets measured, gets managed.Artificial intelligence is the accelerant. AI-enabled drug discovery is compressing timelines for identifying novel longevity compounds from decades to years. Firms like Rejuvenate Biomed are already using AI to recombine existing approved drugs into novel geroprotective formulations, dramatically lowering development risk and time-to-market. The pharmaceutical and biotechnology segment is expected to grow at 10.26% CAGR through 2035 as this commercialization wave intensifies.

A Global Market With a Clear Growth Frontier

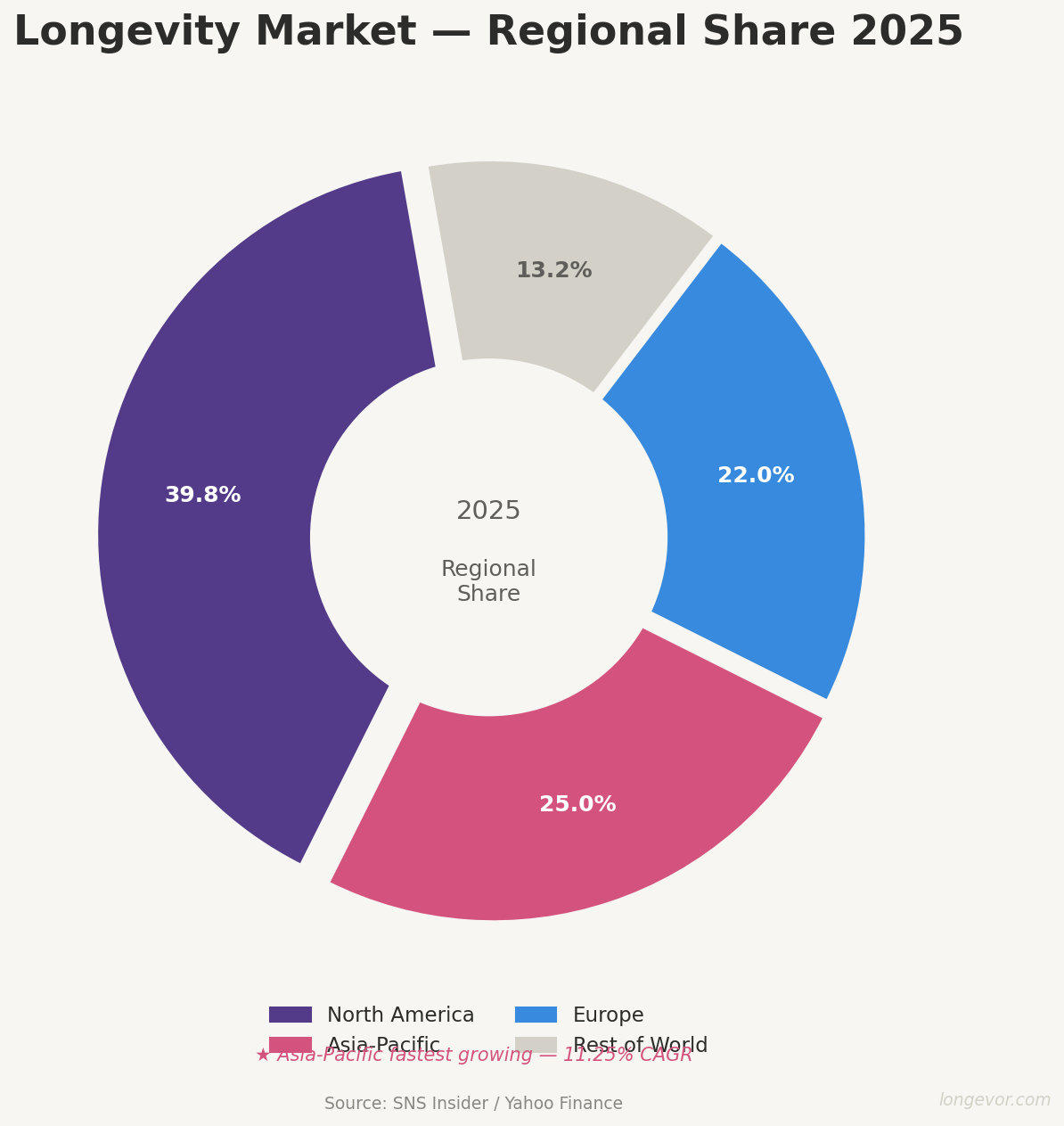

North America remains the dominant force, holding 39.84% of global market share in 2025 supported by the world’s deepest biotech ecosystem, robust venture capital infrastructure, and a consumer base with both the awareness and the purchasing power to act on longevity science.

But the most important growth story is unfolding in Asia-Pacific, which is projected to expand at an 11.25% CAGR — the fastest of any region. Japan, South Korea, and China face among the most acute demographic aging pressures in the world, and they are responding with both government-level investment and explosive consumer adoption. India is entering the picture with purpose: its preventive healthcare market was valued at USD 197 billion in 2025, and the country’s anti-aging services segment is projected to reach USD 1.06 billion by 2035 a signal that longevity is becoming a mainstream priority, not a niche luxury.

The Service Economy of Longevity: Hospitality, Wellness, and Clinical Precision

The longevity market is not only a biotech story. It has spawned a sophisticated ecosystem of high-value service verticals, each redefining what premium health investment looks like.

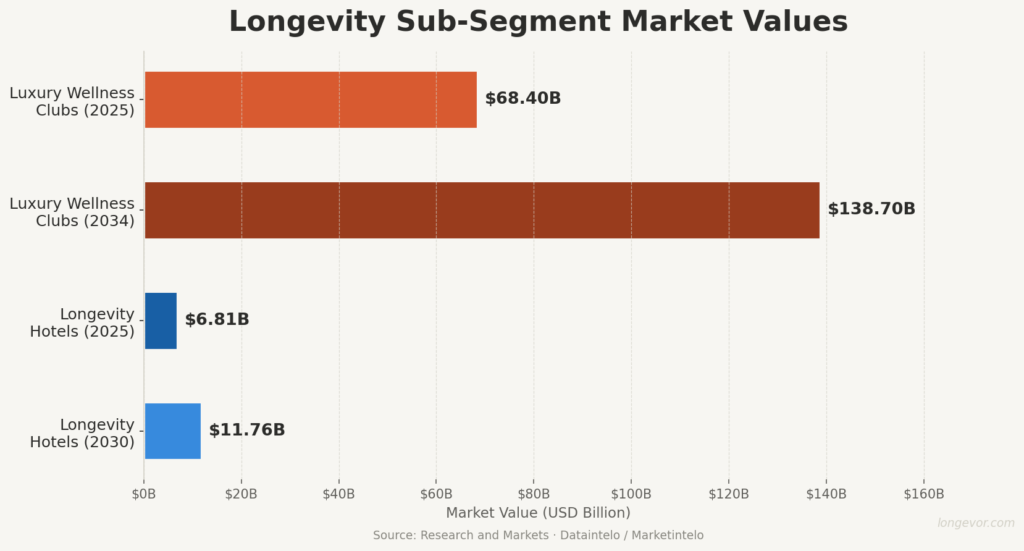

Longevity hotels, combining nutritional genomics, biohacking suites, and medical-grade diagnostics under one roof, were valued at USD 6.81 billion in 2025 and are forecast to reach USD 11.76 billion by 2030 — an 11.5% CAGR that reflects surging demand for immersive, results-driven wellness experiences.

Luxury wellness clubs have undergone a more dramatic reinvention. The global market, anchored by operators like Equinox and Life Time, reached USD 68.4 billion in 2025 and is projected to hit USD 138.7 billion by 2034. The membership model has evolved well beyond fitness: Equinox’s “Optimize” tier, priced at USD 30,000–40,000 per year, integrates biomarker testing and AI-driven health programming. Canyon Ranch and SHA Wellness offer destination memberships reaching USD 150,000 annually. These are not gym memberships. They are longevity infrastructure subscriptions.

At the clinical apex, concierge longevity clinics command annual memberships of USD 25,000 to USD 100,000, delivering 2–8 hours of monthly medical consultation, access to advanced diagnostics including MRI brain imaging and cognitive assessments, and individualized longevity roadmaps. Fortune 500 companies are investing USD 8,000–30,000 per executive for corporate wellness mandates — recognizing that biological performance is an organizational asset.

The Competitive Landscape: Who Is Building the Future of Longevity

The sector is attracting capital and talent at every layer of the stack.

In biotechnology, the foundational work is being done by firms like Altos Labs, Calico Life Sciences, Unity Biotechnology, BioAge Labs, Insilico Medicine, and Human Longevity Inc. — each pursuing distinct but complementary angles on cellular reprogramming, AI-driven drug discovery, and biological age reversal. Pharmaceutical giants AbbVie and Recursion Pharmaceuticals are accelerating their entry into anti-senescence therapeutics, bringing the resources to scale what the pioneers have proven.

In the luxury service layer, operators including Equinox, Life Time, Lanserhof, Chiva-Som, and Canyon Ranch are translating the science into experiential models that serve the 120 million consumers who entered the longevity market by 2025.

The competitive intensity across both layers is high — and will only increase as the market approaches USD 67 billion.

Where Longevor Stands

This market needs more than products. It needs trusted guides — practitioners and platforms that can synthesize the complexity of longevity science into actionable, evidence-grounded protocols that real people can implement.

The proliferation of supplements, diagnostics, clinics, and AI tools creates as much noise as signal. The consumers and professionals navigating this space need clarity on what works, what is validated, and what is built on rigorous science versus marketing.

That is the precise gap Longevor is designed to fill.

We are not passive observers of this industry’s growth. We are participants — committed to elevating the standard of evidence, translating the cutting edge of longevity science into clinical and consumer practice, and building the infrastructure for a future in which extended, optimized healthspan is not a privilege of the ultra-wealthy but a broadly achievable outcome.

The longevity economy is the defining industry of the 21st century. The science is ready. The capital is committed. The consumer demand is proven.

The question now is not whether this transformation will happen — it is who will lead it responsibly.

Longevor is a longevity intelligence platform dedicated to translating the science of aging into practical, evidence-based strategies for extended healthspan. For research partnerships, clinical inquiries, or media requests, contact us at hello@longevor.com.

References

- SNS Insider – Longevity Market Report

- Yahoo Finance – Longevity Market Size Projection

- Research and Markets – Longevity Market Report

- Mordor Intelligence – Longevity Market Analysis

- MarketsandMarkets – Longevity Ingredients Market

- Market Research Future – Longevity Market

- GlobeNewswire – Longevity Market Growth Report

- Healthy Longevity Clinic – Prague

- HolonIQ – Longevity Deep Dive

- DataIntelo – Luxury Wellness Club Membership Market

- SSRN – Longevity Research Paper